- Your Government

-

Our Community

-

- About St. Helens History of St. HelensState of the CityCourthouse Dock Camera

- Local Events City Calendar Citizens Day in the ParkRecreation Activities Discover Columbia County Sand Island CampingKeep It Local CC

- Community Resources City Newsletter City Social Media Emergency Services New Resident InformationProtecting Our Environment

-

-

Business & Development

-

- Local Business Directory Get a Business License City Bids & RFPs Broadband Study

- Business in St. Helens St. Helens Advantages Directions & Transportation Incentives & Financing Resources for Businesses Business Guide Columbia Economic Team Chamber of Commerce

- Current City Projects Waterfront Redevelopment Public Safety Facility Strategic Work Plan

-

-

How Do I?

-

- Apply for a Job Apply for a Committee Find A Park Find COVID Info Find Forms Follow St. Helens - Facebook Follow St. Helens - Twitter Follow St. Helens - YouTube

- Get a Police Report Get a Business License Get a Library Card Get a Building Permit Newsletter Signup Past Public Meetings Pay My Water Bill

- Public Records Request Report a Nuisance Register for Rec Activity Reserve a Park Sign Up for the 911 Alerts Universal Fee Schedule

-

Incentives & Financing

Business Oregon Programs

Business Oregon has a team of professionals to assist businesses with their financing needs by packaging loan programs or by matching a partner service provider with a business. Business Oregon manages the following financing programs to assist businesses:

- Oregon Business Development Fund

- Oregon Capital Access Program

- Oregon Credit Enhancement Fund

- Oregon Industrial Development Bonds

- Entrepreneurial Development Loan Fund

- Business Retention Program

- Brownfields Redevelopment Fund

- Oregon New Market Tax Credit

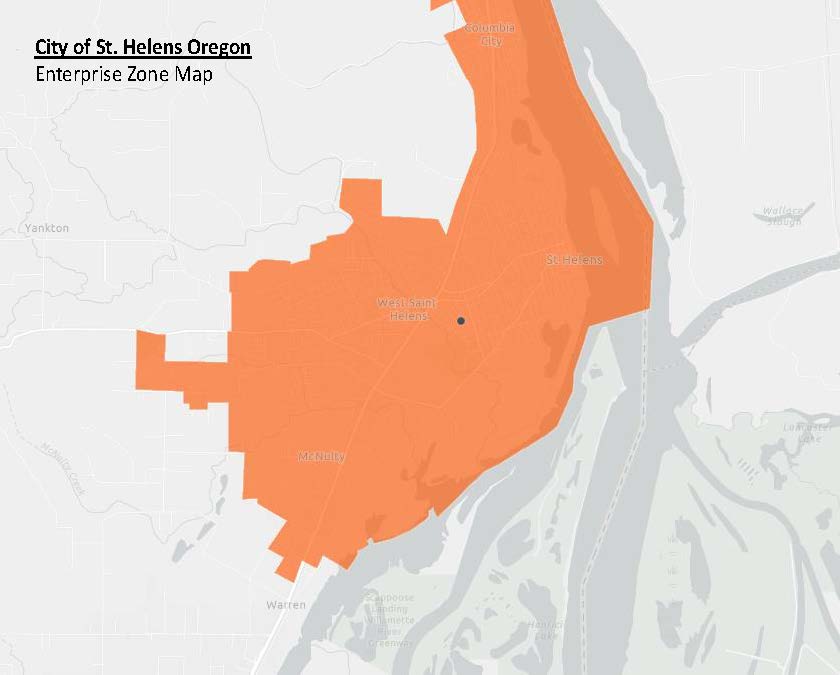

Enterprise Zone

St. Helens offers a property tax abatement program that provides a property tax exemption for industrial businesses and certain hotel/motel facilities that make a minimum of $50,000 of new investments in real property and/or equipment and create new jobs. Check the attached map to see if your business location may qualify for Enterprise Zone Benefits.

For additional & more detailed information, please check out the Business Oregon site on Enterprise Zones; BUSINESS OREGON ENTERPRISE ZONE

How it Works

In exchange for locating or expanding into an enterprise zone, eligible (generally non-retail) business firms receive total exemption from the property taxes normally assessed on new plant and equipment for at least three years, but possibly up to five.

Eligible Businesses

Eligible businesses must produce, sell, or provide goods, commodities, products, merchandise, work, or services to other businesses or business operations. This includes conventional manufacturing, as well as assembly, fabrication, processing, shipping or storage, warehouse, distribution, bulk clerical processing, printing or mass document production, after-sale technical support, and maintenance facilities. Industrial processes such as cleaning, coating, curing, kiting, labeling, laminating, packaging, refining, smelting, sorting or treating are eligible, as is development of standardized computer software products. Call centers in which no more than 10% of the customers or business transactions come from inside the local calling area, in which the telephone calls are made without long distance charges can be eligible if they meet certain additional requirements. Hotels and Motels including associated property of ancillary operations are eligible under the motel/hotel option if used 50 percent or more by overnight guests.

Qualified Property

- Minimum $50,000 investment.

- Real property such as newly constructed buildings or structures.

- New additions or modifications to existing building/structure.

- Heavy/affixed machinery and equipment.

- Machinery and equipment classified as personal property (readily movable) $50,000 or more.

Not eligible: land, non-inventory supplies, rolling stock, vehicles, motor-propelled devices, and certain minor personal property items.

Program Options

3-Year Enterprise Zone Tax Exemption

- Invest at least $50,000 in new plant or equipment.

- Increase full time permanent employment by the greater of 1 person or 10% of existing employment base.

- Pay the new employees an average of 150% of minimum wage (2017: $16.87 per hour). Most benefits can be used to meet this total compensation level.

- Maintain increased employment level over 3 years.

- Enter into a First Source Hiring Agreement with local job training providers. Commits company to consider local applicants for new hires.

- Complete intake application and pay $200 fee before proceeding with the program.

5-Year Enterprise Zone Tax Exemption

- Invest at least $50,000 in new plant or equipment.

- Increase full time permanent employment by 10% of existing employment base.

- Pay the new employees an average of 100% of average Washington County (2017: currently $65,908) yearly wage. Most benefits can be used to meet this total compensation level.

- Maintain increased employment level and wage over 5 years.

- Enter into a First Source Hiring Agreement with local job training providers. Commits company to consider local applicants for new hires.

- Complete intake application and pay application fee of .001% of the total investment capped at $25,000 before proceeding with the program.

- Pay community service fee equal to 25% of the value of the abated tax in each of years four and five.

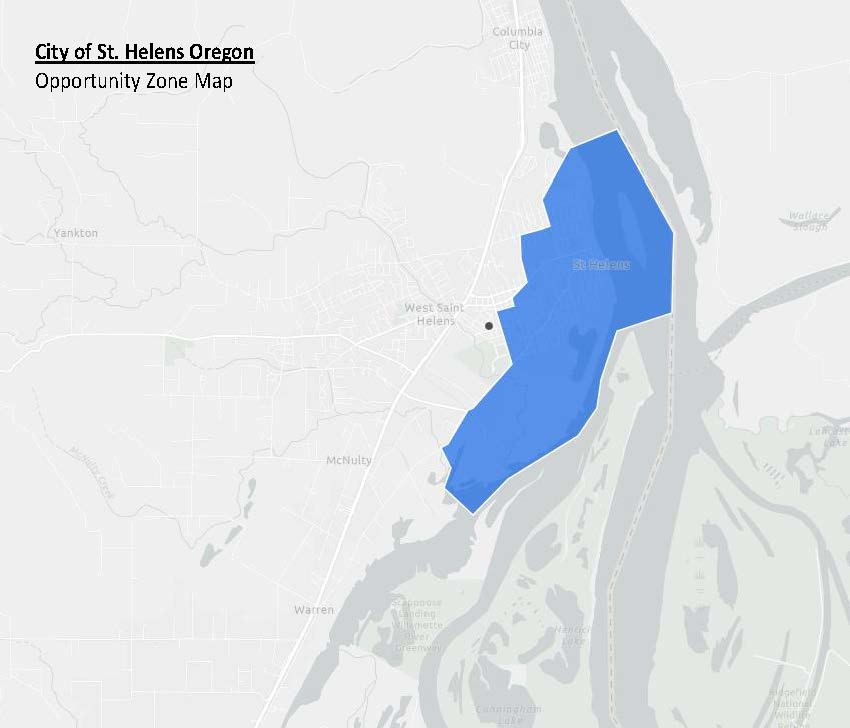

Opportunity Zone

In 2018, the U.S. Treasury made opportunity zone designations across the country to encourage long-term investments through a federal tax incentive. Governor Brown's nomination resulted in 86 qualified opportunity zones in Oregon. St. Helens is one of those zones (Tract #9707).

For additional & more detailed information, please check out the Business Oregon site on Opportunity Zones; BUSINESS OREGON OPPORTUNITY ZONE

How it works

The private capital for projects or businesses in a qualified opportunity zone will arise primarily from the unrealized capital gains of U.S. taxpayers—that is, the increased value of assets (stocks, land, etc.) since they were originally purchased by the individual or corporation currently holding the asset. When an asset is sold and the gains realized, an income tax liability is normally generated.

With the opportunity zone incentive, the capital gains arising from sale to an unrelated person that are then transferred into a qualified opportunity fund within 180 days will have their tax liability delayed or deferred. The taxpayer decides how much of their newly realized gains to invest, when to sell or exit that investment, or even whether to invest other moneys alongside (which would not receive these tax benefits).

In addition to deferring income taxes, by the time the investment of tax-deferred capital gains in the opportunity zone is sold:

The amount subject to taxes shrinks by 10%—in that the basis in the investment increases—if the investment has been held for at least five years. If held for at least seven years in total, the basis increases by an additional 5% pts (15% in total). The amount subject to taxes is effectively the fair market value of the investment, if it has declined in value.

If the value of the original investment of capital gains appreciates after having been held for at least 10 years in the QOF, then those new capital gains earned in the zone are themselves completely tax free. Otherwise, the net income or proceeds generated by a zone investment are taxable. This 10-year hold on the investment in the QOF must begin on or before December 31, 2026, and the investment or interest in the QOF must be disposed of or liquidated or the gains realized on or before December 31, 2047.

Investors seeking to maximize the after tax return on their tax deferred gains could put money into qualified opportunity zones anywhere in the country, or they might be able to choose qualified opportunity funds that have a regional or other type of emphasis. Despite sharing some common geography, these tax benefits work quite differently from New Market Tax Credits, or for that matter, from any other federal program or incentive. Regulations and other guidance issued by the Internal Revenue Service (IRS) have now addressed most of the critical details, although future issuances are still expected and proposed rules are still to be officially finalized.

What are Qualified Opportunity Funds (QOF)?

A Qualified Opportunity Fund is the required vehicle to invest into Opportunity Zones. Click here for more information on opportunity funds.

{kind=link}

{kind=link}